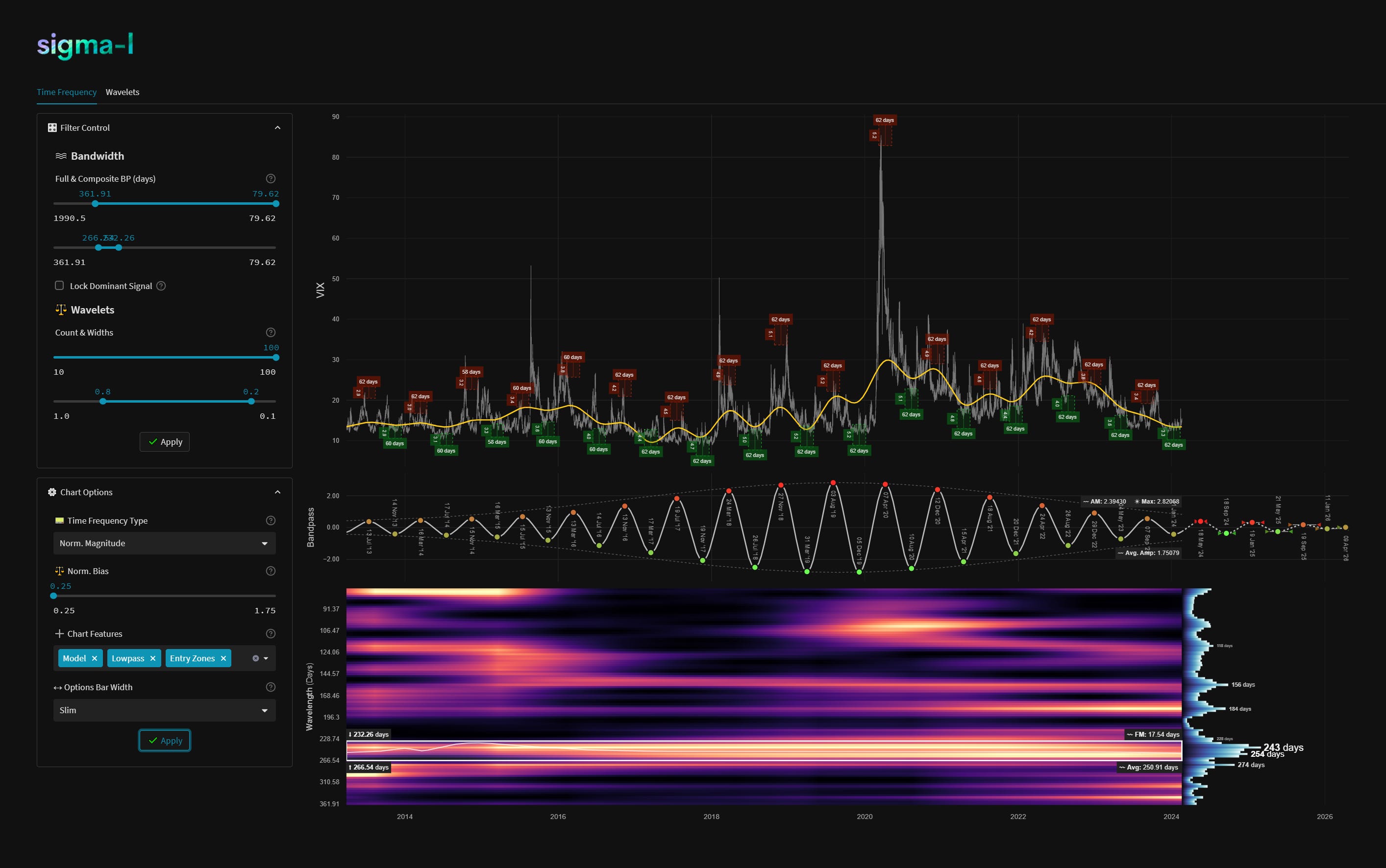

CBOE Volatility Index (VIX) - 19th February 2024 | @ 251 Days

'B' class signal detected in CBOE Volatility Index (VIX). Running at an average wavelength of 251 days over 16 iterations since April 2013. Currently turning up.

ΣL Cycle Summary

It should perhaps come as no surprise to readers, having seen the excellent out of phase correlation in the VIX to the 80 day nominal wave in stock markets, that there is also a similar wave around 250 days - married inversely to the 40 week nominal wave in stock markets. In this new addition to Sigma-L we look at the quality of the longer term signal using our usual tools to establish the current phase. It is certainly one of the most powerful signals in a bandwidth from around 360-90 days, providing impetus down the spectra to the shorter components, spiking to the upside when markets move sharply down. Crucially any modulation is minimal, as shown below, with a perfectly acceptable average error range of +- 17 days for each estimated peak and trough, equating to 6.7% of the average wavelength at 251 days.

Time Frequency Analysis

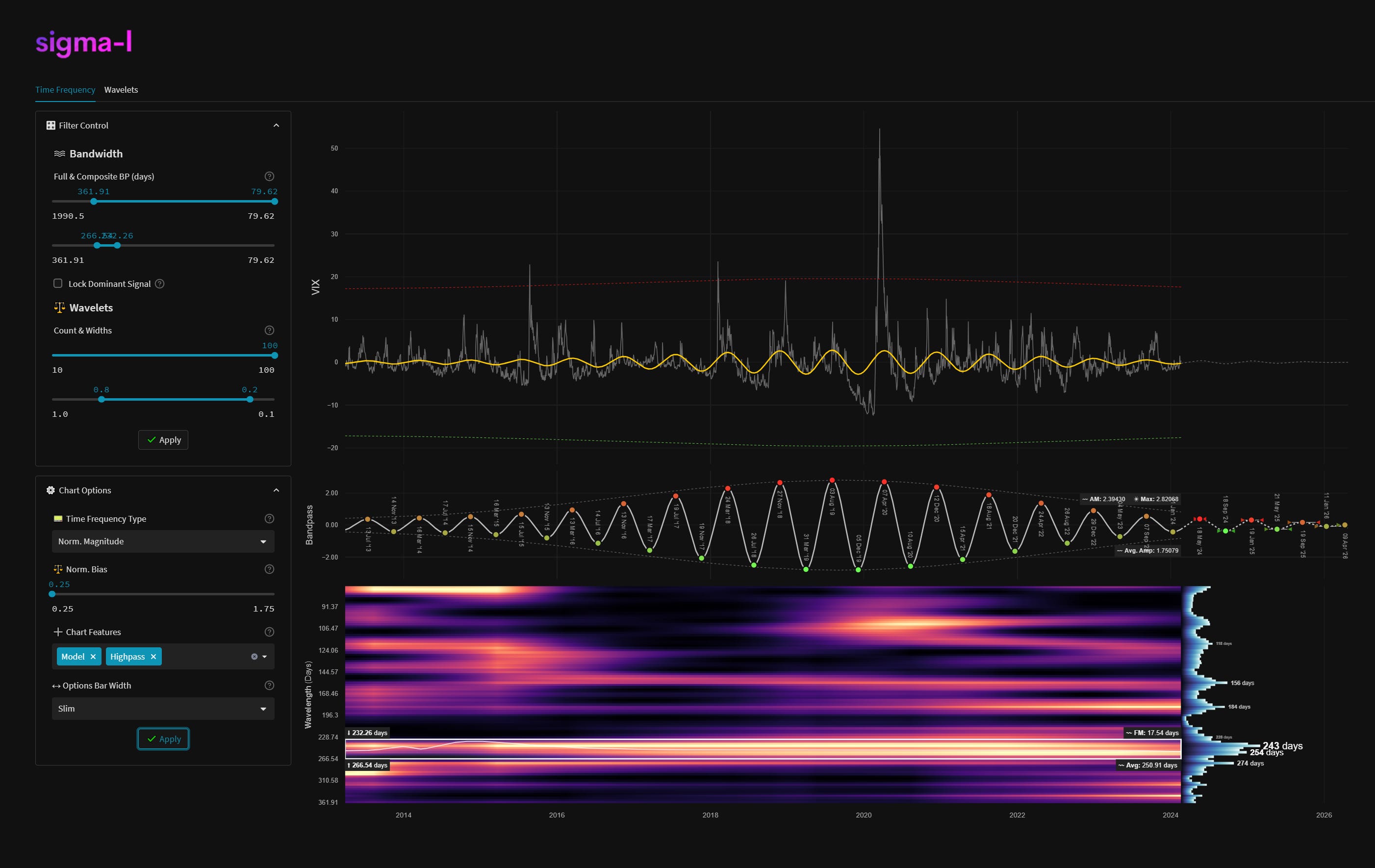

Time frequency charts (learn more) below will typically show the cycle of interest against price, the bandpass output alone and the bandwidth of the component in the time frequency heatmap, framed in white. If a second chart is displayed it will usually show high-passed price with the extracted signal overlaid for visual clarity.

Current Signal Detail & Targets

Here we give more detail on the signal relative to speculative price, given the detected attributes of the component. In most cases the time target to hold a trade for is more important, given we focus on cycles in financial markets. Forthcoming trough and peak ranges are based upon the frequency modulation in the sample (learn more).

Detected Signal Class: B - learn more

Average Wavelength: 250.91 Days

Completed Iterations: 16

Component Yield Over Sample: 853.20% - learn morePhase: Turning Up

FM: +- 17 Days

AM: 2.34430

Next Trough Range: 1st September - October 5th, 2024

Next Peak Range: 1st May - 4th June, 2024

Sigma-L Recommendation: Late Buy

Time Target: ~ 18th May, 2024

Current Signal Phase

This is ‘how far along’ the cycle is in it’s period at now time and is related to the predicted price action direction.

Current Signal Frequency Modulation (FM)

This is how much, on average, the signal detected varies in frequency (or wavelength) over the whole sample. A lower variance is better and implies better profitability for the component. Frequency usually modulates relatively slowly and over several iterations.

Current Signal Amplitude Modulation (AM)

This is how much the component gains or loses power (price influence) across the sample, on average. Amplitude modulation can happen quite quickly and certainly is more evident than frequency modulation in financial markets. The more stable the modulation the better.