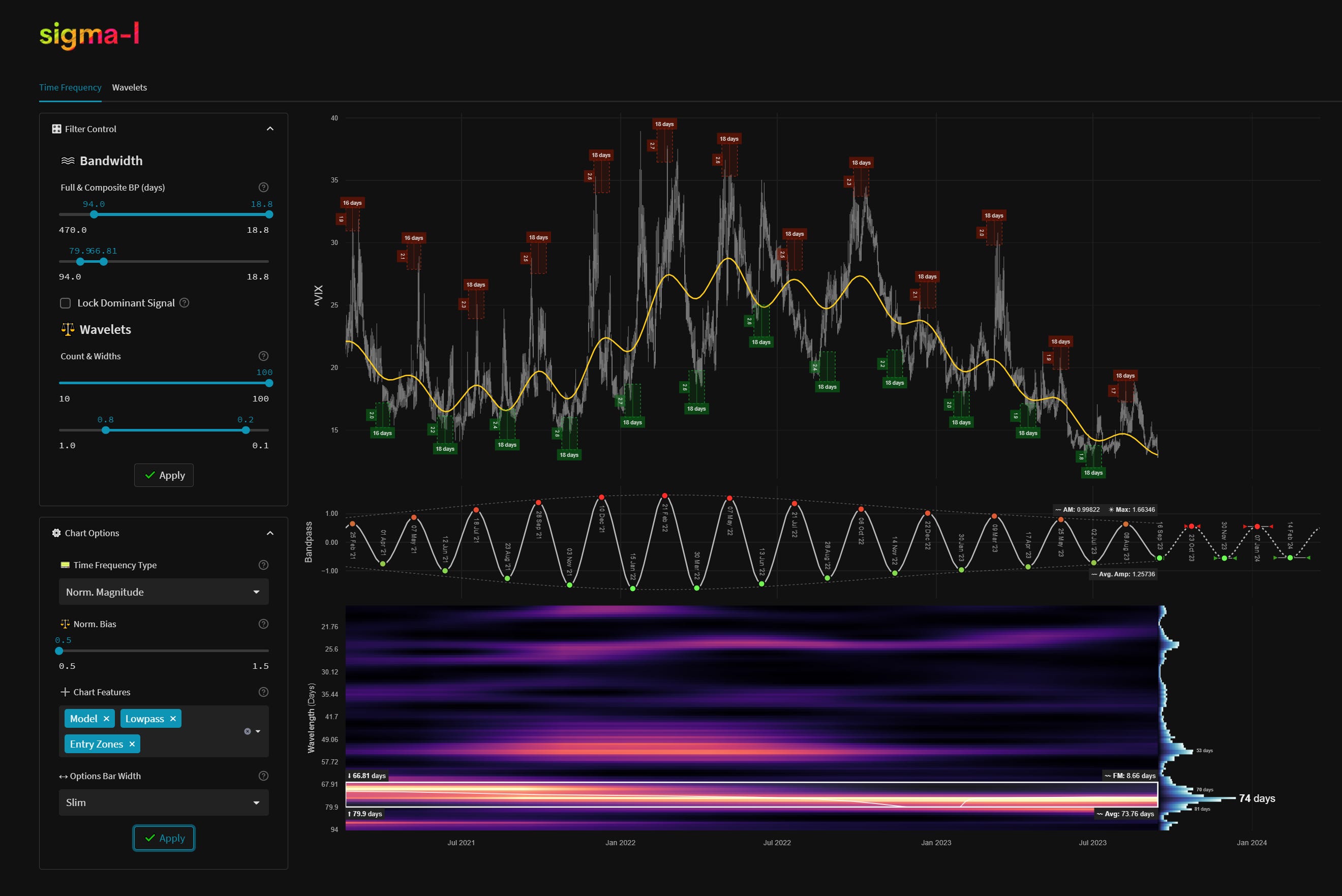

CBOE Volatility Index (VIX) - 15th September 2023 | @ 74 Days | + 20.11%

Last trade: + 20.11% | 'B' class signal detected in CBOE Volatility Index (VIX). Running at an average wavelength of 74 days over 13 iterations since February 2021. Currently troughing.

Trade Update

See also: Live ΣL Portfolio & History

Summary of the most recent trade enacted with this signal and according to the time prediction detailed in the previous post for this instrument, linked below.

Type: Sell - CBOE Volatility Index 9th August 2023

Entry: 9th August 2023 @ 15.96

Exit: 15th September 2023 @ 12.75

Gain: 20.11%

Current Signal Status

Defining characteristics of the component detected over the sample period.

Detected Signal Class: B - learn more

Average Wavelength: 73.76 Days

Completed Iterations: 13

Time Frequency Analysis

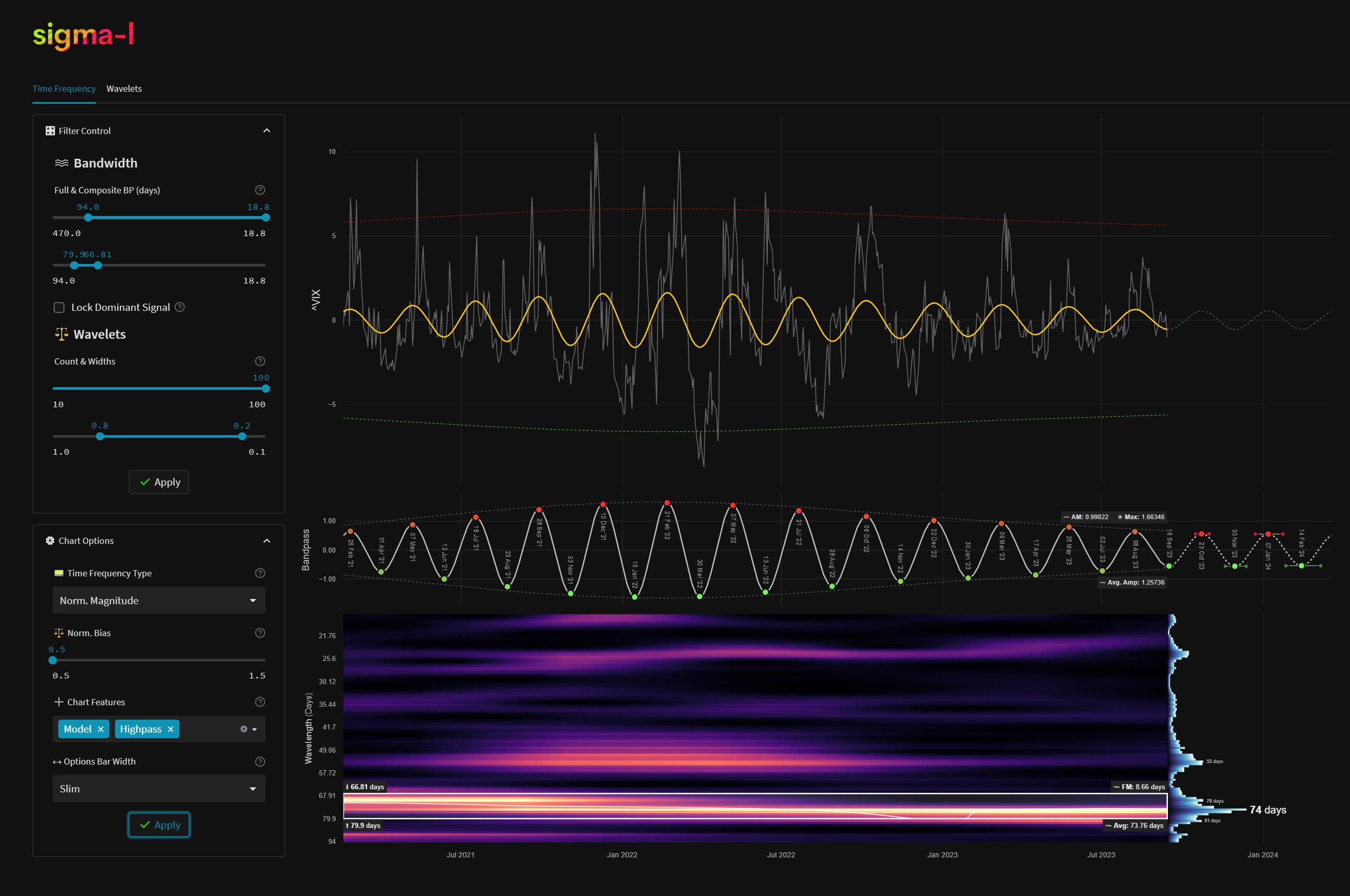

Time frequency charts (learn more) below will typically show the cycle of interest against price, the bandpass output alone and the bandwidth of the component in the time frequency heatmap, framed in white. If a second chart is displayed it will usually show highpassed price with the extracted signal overlaid for visual clarity.

Current Signal Detail & Targets

Here we give more detail on the signal relative to speculative price, given the detected attributes of the component. In most cases the time target to hold a trade for is more important, given we focus on cycles in financial markets. Forthcoming trough and peak ranges are based upon the frequency modulation in the sample (learn more).

Phase: Troughing / Troughed

FM: +- 9 Days

AM: 0.99822

Next Trough Range: 21st November - 9th December, 2023

Next Peak Range: 14th October - 2nd November, 2023

Sigma-L Recommendation: Buy

Time Target: ~ 23rd October, 2023

Current Signal Phase

This is ‘how far along’ the cycle is in it’s period at now time and is related to the predicted price action direction.

Current Signal Frequency Modulation (FM)

This is how much, on average, the signal detected varies in frequency (or wavelength) over the whole sample. A lower variance is better and implies better profitability for the component. Frequency usually modulates relatively slowly and over several iterations.

Current Signal Amplitude Modulation (AM)

This is how much the component gains or loses power (price influence) across the sample, on average. Amplitude modulation can happen quite quickly and certainly is more evident than frequency modulation in financial markets. The more stable the modulation the better.